🔦 The Search

Search funds as an alternative asset class, giving up on AI content on an aged domain and more details on VALT's Portfolio Construction

Last week’s newsletter on HoldCos and entrepreneurship through acquisition seemed to resonate well.

In fact one subscriber John Gillham from websiteincome.com (who I interviewed 18 months ago on the Website Investing podcast) reached out to let me know that he’s now buying up businesses in his local area through his HoldCo, Escarpment Capital.

It really does just make sense, reinvesting money made online into offline businesses, whilst adding online acquisition channels to them.

I’ve since had a meeting with a local accountant about structuring the HoldCo, and whether it’s better to acquire through a share or asset sale.

We then talked about due diligence. I sent out this tweet over the weekend as wasn’t sure in the offline world what services are out there:

It seems the answer, at least in the UK, is within corporate finance teams within larger accounting firms, i.e. I’ve not been able to find a Flippa Due Diligence style service for offline acquisitions.

The first deal I was looking to do was a cafe I go to where the owner is looking to retire. I have an investor partner, who bought my software review site back in the day, and we’ve built trust (and a friendship) through acquiring and building other sites together.

Together we proposed a small up front payment with majority seller financing paid out from the profit of the business. The owner would get paid interest for the loan and end up receiving more than the asking price over time.

The owner has countered with an all up-front offer which (being multiple six figures) would be too much for myself and investor partner to stomach. I looked at bringing in other investor friends, who were keen, and I think I could get to the full amount.

However, I’ve realized that our equity (at 25% each) would be too small to be material for the cashflow from a business this size. The ROI becomes longer and smaller. Plus, at the current level of EBITDA it would take over 4 years for an investor to make their money back at current profit levels.

Whereas with majority seller financing it halves the time to get cash back, and halves the number of investors required (you’re able to leverage the return on equity invested).

This is why search funds don’t target main street businesses (revenues up to $2MM).

Search fund model

The searcher of a search fund actually does end up with 25% equity (or less) as the fund looks to acquire a much larger business within the lower middle market ($5MM-$50MM revenue).

And the trend I’m seeing is that search funds are becoming more interested in moving from traditional, off-line (‘boring’) businesses, to acquiring online businesses on platforms like Flippa, as it moves into listing more 7 and 8 figure assets. You can read about the off-market app portfolio that recently sold on Flippa for $35MM.

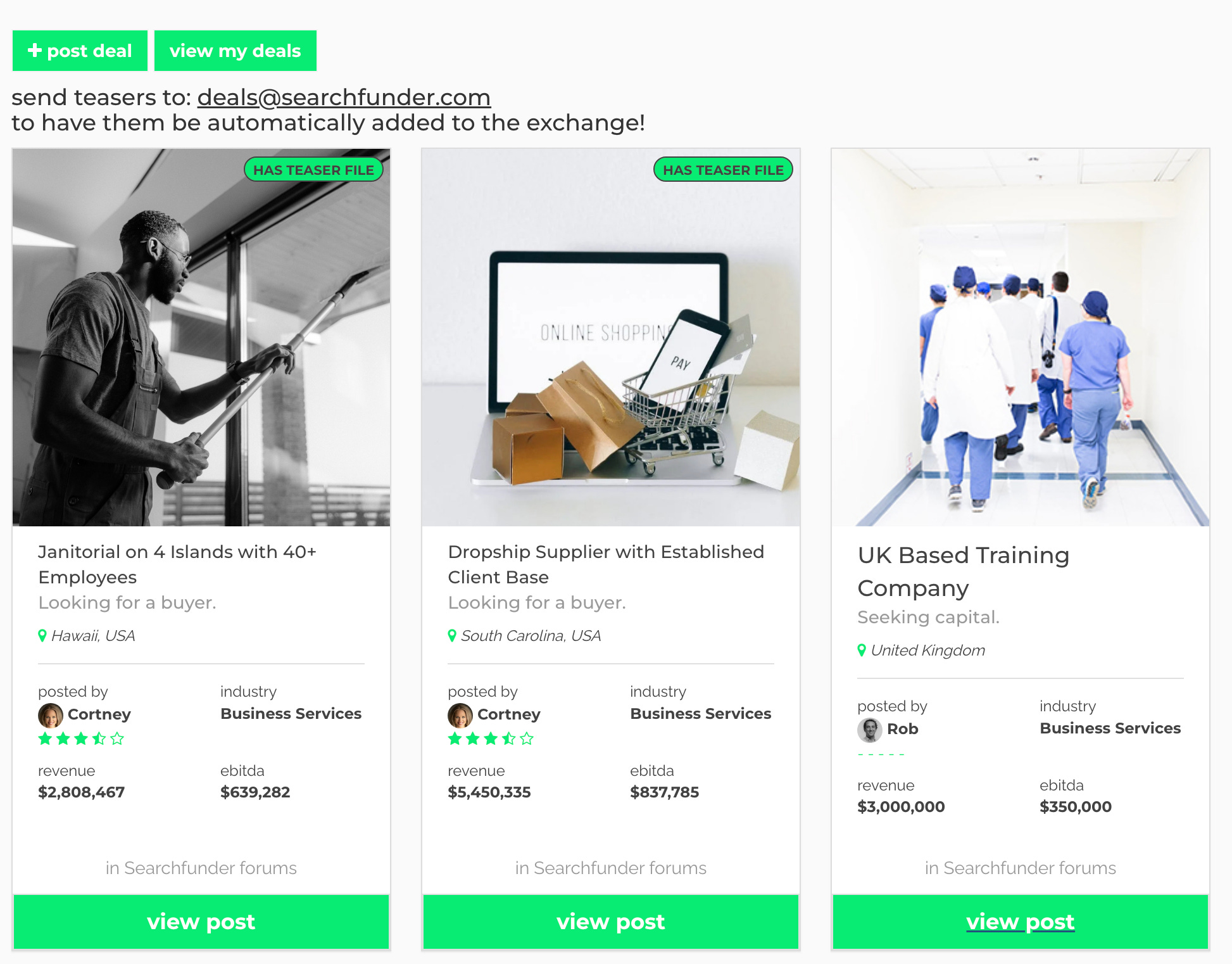

There is a platform for search funders, based out of Portland, Oregon (boy do I miss Pips donuts - if I lived there I’d want to buy it!) called searchfunder.com by founders Mark & Luke. It lists deals that people post who are looking for investors:

Investing in search funds

If you’re interested in investing in a search fund, there’s a wealth of information in the Search Fund Primer by Stanford Graduate School of Business, from formation documents to due diligence topics. It’s from the perspective of the entrepreneur raising a fund from investors but it’s interesting how it states:

An investment in a search fund falls into the alternative asset class, which typically makes up 5 to 15 percent of an individual’s investment portfolio.

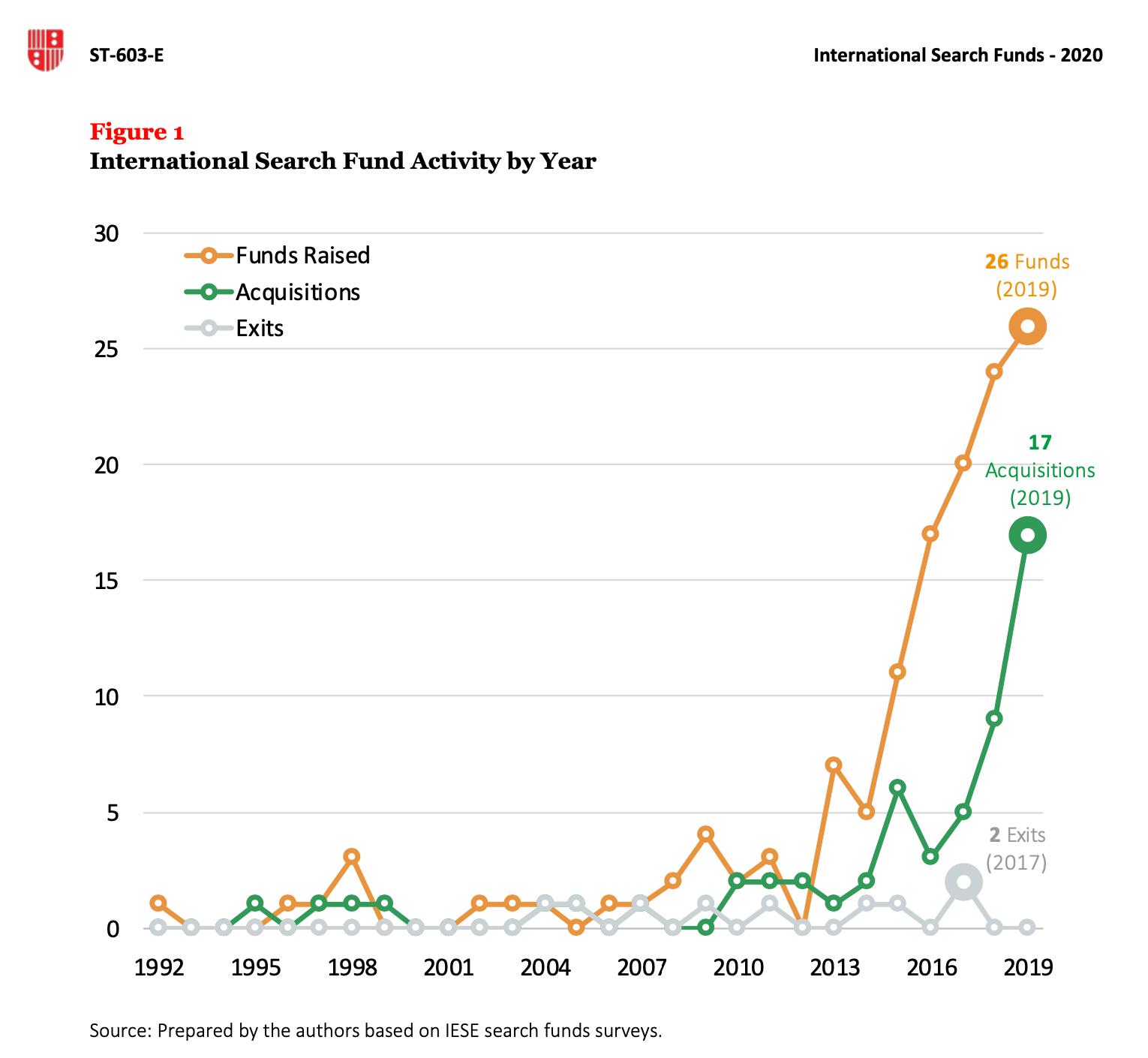

Another good resource is the International Search Funds 2020 report by IESE Business School. 2019 is the last data point but it shows the trajectory of overseas search funds (with the first one being raised in the UK) - it’s no longer just a US concept:

A great recent podcast on searching is by Michael Girdley talking with Steve Ressler of Brydon Group:

And Michael was just on the My First Million podcast talking with Shaan Puri and Sam Parr about his $100MM+ revenue HoldCo that has 15-20% EBITDA margins which is mainly reinvested and compounded:

#contentsites

Those who have been following along pre the Flippa acquisition may remember (here and here) that I was trying to build a new authority site (in the poker niche) using AI written content on an aged domain from Odys.

Unfortunately we just couldn’t get the site to index properly, in a very similar way to Spencer’s experience below:

As such the site has been abandoned / returned to Odys and unfortunately no interesting case study will be happening about an exit on Flippa!

#fractional

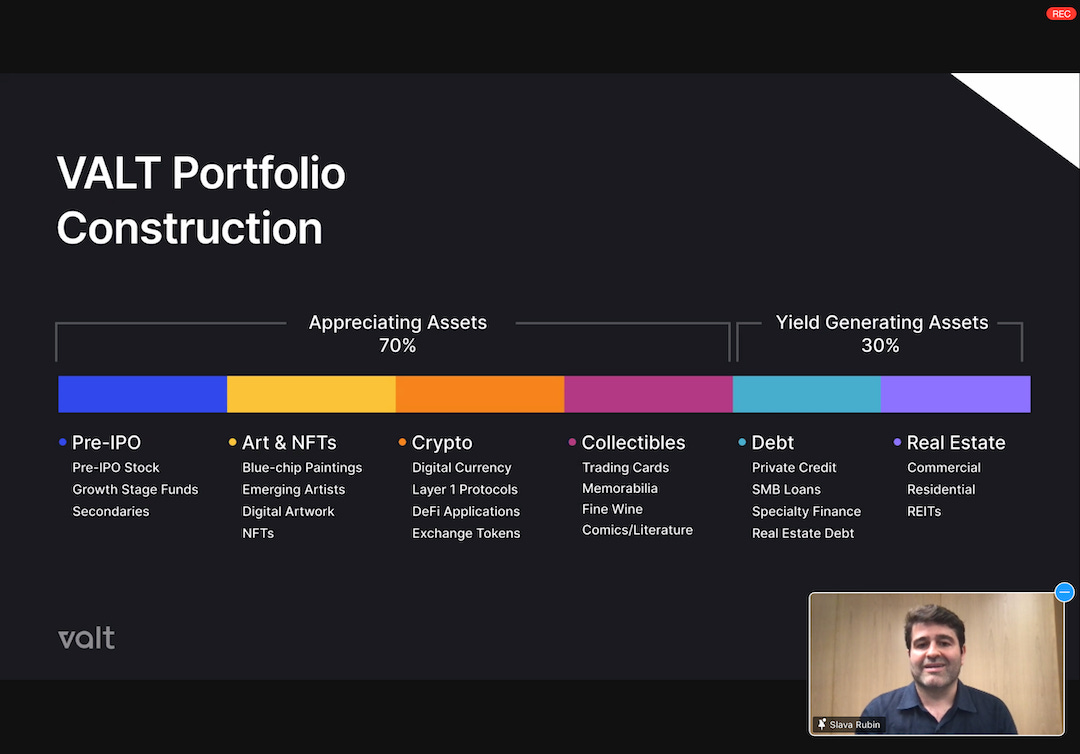

I was just on a webinar with Slava Rubin from Vincent about their new VALT fund. It’s across 6 different alternative asset classes with 70% being appreciating assets and 30% yield generating assets:

Perhaps online businesses assets, that can be a combination of growth and yield, in the hands of the right operator, will be included in their next fund.

Ok that’s it for this week. If you’re reading this on the web and you’re not yet subscribed just hit the button below.

And come join over 1400 members in the Alts by Flippa Community:

Alts by Flippa is owned by Flippa. Nothing in this email is financial advice and we are not professional investment advisers. We send weekly updates on what we're doing personally - consider it informational and for entertainment purposes only.